Fake loan text scams are one of the most widespread SMS fraud patterns targeting people in the UK and US right now. They arrive without warning, claim you've been pre-approved for a large personal loan you never applied for, and pressure you to click a link or call back immediately. No loan exists. The only goal is to steal your personal information, your money, or both.

"CNFI USA" is the most consistently reported name behind these texts, with new complaints filed as recently as March 2026 — this is an active, ongoing campaign, not a closed case. The operation behind it may eventually shift to other invented names, but the phone numbers, the "Alexis" persona, and the script itself stay recognisable regardless of which name is attached.

You get a text out of nowhere. You're pre-approved for a personal loan — great rate, instant decision, just click the link. It looks official. It feels urgent.

It's a scam.

This guide explains exactly how fake loan text scams operate, which names and aliases they commonly use, the red flags that give them away immediately, and what to do if you've already responded.

What Is the CNFI USA Fake Loan Text Scam?

"CNFI USA" is not a real lender. It's a name used by scammers to make a fraudulent text look like it's coming from a legitimate financial company. The goal of these messages is almost always one of two things:

- Steal your personal information — name, address, Social Security number, bank details

- Charge you an upfront "processing" or "activation" fee — which you'll never see again

The messages are designed to look credible. They use professional language, reference loan amounts, and often claim you've already been approved — even though you never applied for anything.

The Name Isn't the Point

Scammers running fake loan text operations rotate through invented company names to avoid accumulating negative search results and to stay ahead of spam filters. "CNFI USA" is by far the most widely reported name behind this specific script — the same phone numbers, the same "Alexis" persona, and the same wording keep showing up under that label across hundreds of BBB and ScamPulse reports filed between 2025 and early 2026.

Other loan-text operations use entirely different invented names, and names shift over time as old ones attract too many complaints. If the text you received uses a name that isn't "CNFI USA," search it directly on the BBB Scam Tracker (bbb.org/scamtracker) and ScamPulse.com — both update faster than official regulator databases and will usually confirm whether other people have reported the same wording.

The giveaway is never the company name. It's always the combination of: a loan you didn't apply for, a pre-approval you didn't seek, and a link or callback number as the only way to proceed. That structure is the scam, whatever name it's running under.

What the Text Actually Says

The wording is close to identical across hundreds of independent reports — which is itself a tell. A real lender's outreach varies. A script running at scale doesn't.

The message almost always opens with your first name, introduces "Alexis" as the sender, and references a loan request you never made — quoting a specific round dollar amount, most commonly somewhere between $30,000 and $140,000. It typically includes a line close to "pre-approved... perfect for simplifying your finances," asks if you're available to talk, then closes with a callback number and a note that you can text to opt out.

If you don't reply, a second message tends to follow a day or two later — a soft check-in asking whether you saw the first one and whether now is a better time to talk.

Some recipients report the exact same script arriving as a phone call instead of, or in addition to, the text — always from someone introducing themselves as "Alexis," though the actual voice varies between calls. Treat those calls exactly the same as the text: don't confirm any details, and don't ask to be removed from the list. Just hang up and block.

Numbers Reported So Far

The number that shows up most often across current reports is (844) 699-3623, with (877) 274-3096 appearing less frequently. Messages have also been traced to short code 40158.

Blocking these specific numbers won't protect you long-term — operations like this rotate numbers constantly, and a new one can be active within days of the old one getting flagged. Treat this list as a way to confirm you're looking at the same scam, not as something to rely on for filtering.

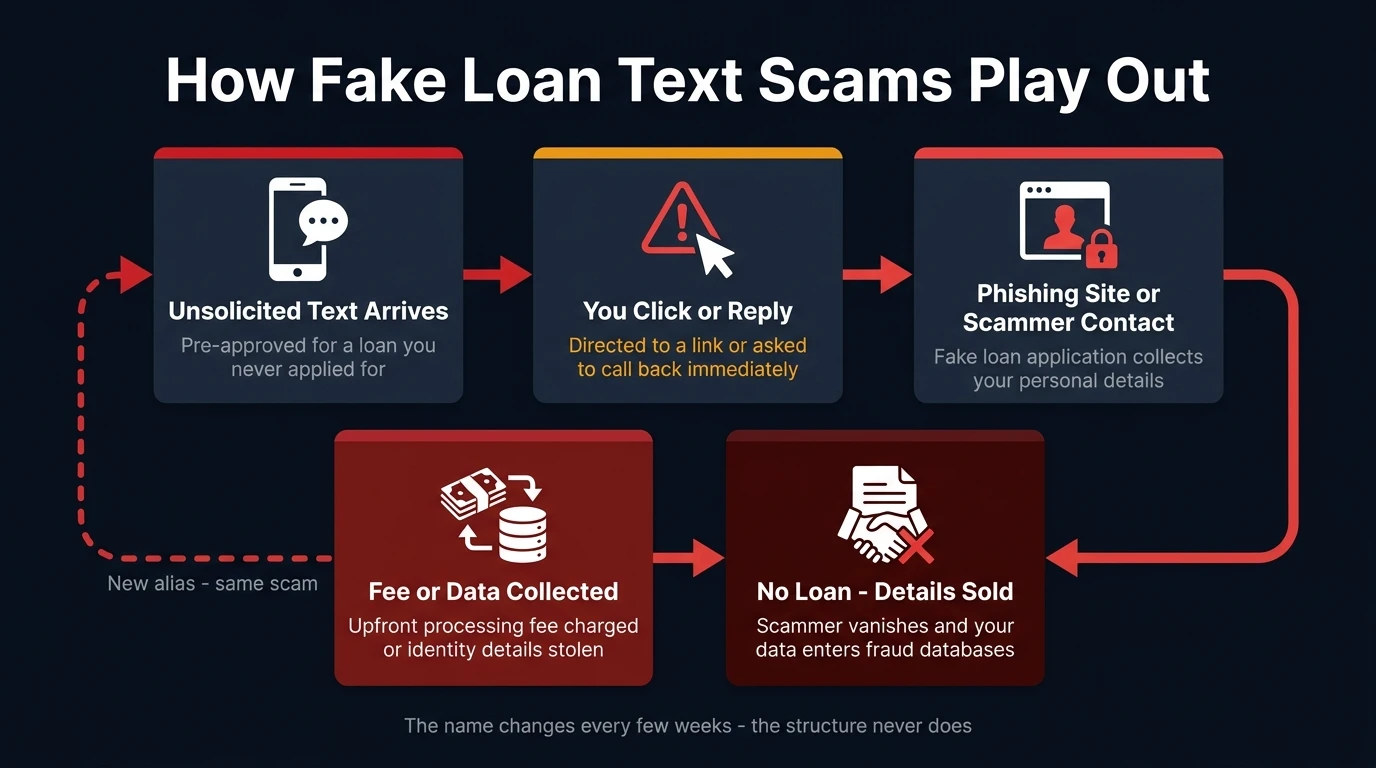

How the Scam Plays Out

The typical sequence goes like this:

- You receive an unsolicited text claiming you're pre-approved for a loan

- You're directed to click a link, reply with your details, or call back to "claim" the offer

- If you click, you land on a phishing site that collects your personal or financial information

- If you reply or call, a scammer — often introducing themselves as "Alexis" — follows up by phone to request fees or more sensitive data

- No loan ever materialises — and your details have been handed to fraudsters

The pressure to act fast is deliberate. Every element of the message — the urgency, the "limited time" framing, the friendly tone — is designed to stop you from pausing to check whether it's real.

Loan Text Scams in the UK

While "CNFI USA" targets US recipients primarily, the UK has its own well-documented variants of the same fraud. In the UK, fake loan text scams most commonly take one of two forms:

Advance fee fraud. You receive a text claiming you've been approved for a loan — often £5,000 to £50,000 — and that to release the funds you must first pay an upfront fee: framed as insurance, processing, or legal clearance. Once you pay, the scammer disappears. The FCA explicitly states that no legitimate UK lender will ever ask for an upfront fee before releasing a loan.

Cloned lender impersonation. Scammers create texts, websites, and sometimes even postal letters that mimic the branding of real FCA-regulated lenders. The contact details go to the scammers, not the real company. Common targets for impersonation include well-known high-street banks and legitimate online lenders.

The UK-specific warning signs are the same as elsewhere — unsolicited contact, upfront fee requests, urgency — but the reporting and verification routes differ:

- Check the FCA register before engaging with any lender: register.fca.org.uk. All authorised UK lenders must be listed.

- Report to Action Fraud: actionfraud.police.uk or 0300 123 2040

- Report to the FCA if a firm is impersonating a regulated lender: fca.org.uk/consumers/report-scam-us

- Forward the text to 7726 — free on all major UK networks including EE, O2, Vodafone, and Three

- Register with CIFAS Protective Registration if your details have been compromised — this makes it harder for fraudsters to take out credit in your name

The same scam infrastructure increasingly targets both countries simultaneously, with slight variations in the loan amounts and company names used. If you're in the UK and receiving texts claiming to be from a US-sounding lender, that alone is a red flag — UK-regulated lenders will always be findable on the FCA register.

For more on government-impersonation text scams specifically targeting UK residents, see our guide to DWP scam text messages and how to spot them. And if the initial text leads to follow-up phone calls — which is common with this type of fraud — see how to handle spam calls from fake debt collectors for what to do when they escalate to voice.

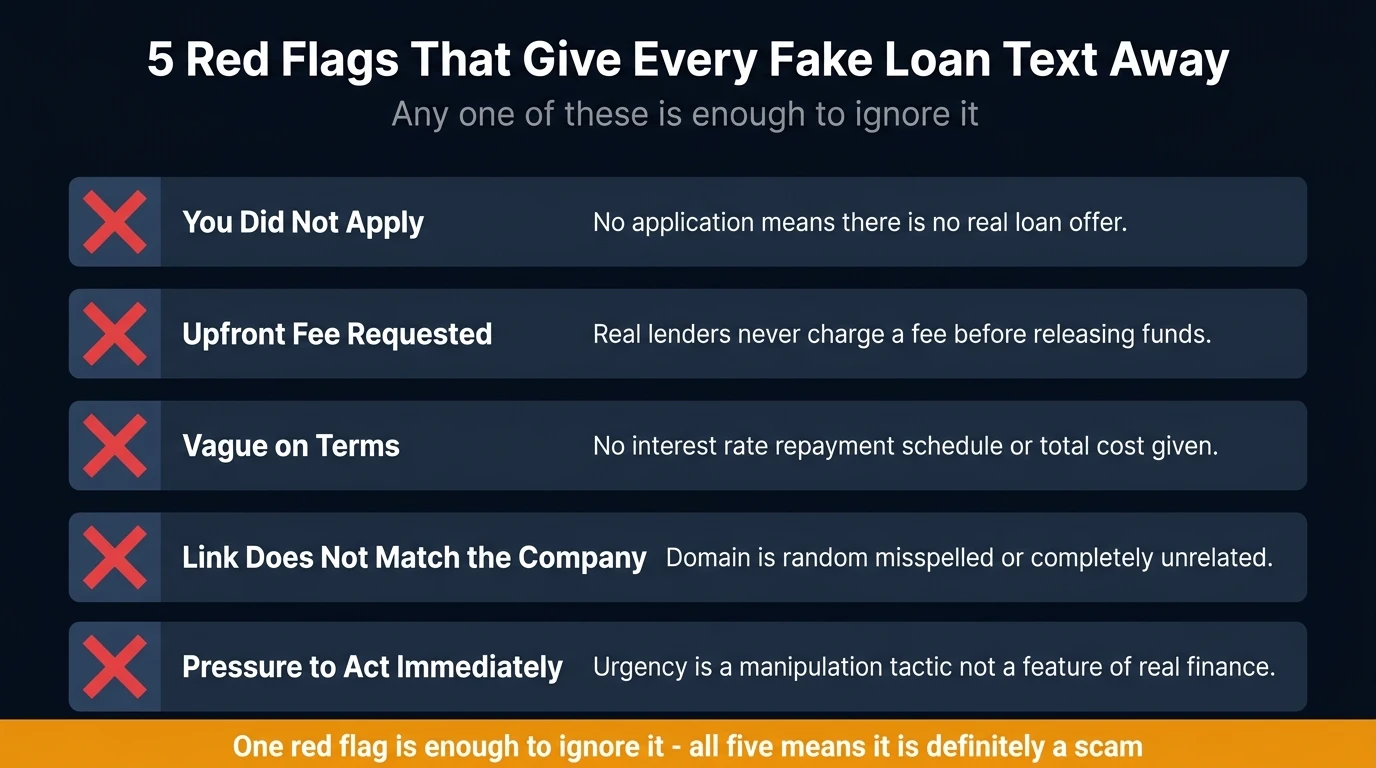

The Red Flags That Give It Away

You don't need to be a fraud expert to spot these. The pattern is consistent:

You didn't apply. If you didn't request a loan, there is no loan offer. Legitimate lenders don't cold-text strangers with pre-approvals.

They want an upfront fee. Real lenders do not ask for a processing fee, activation fee, or insurance payment before releasing funds. This is the single clearest sign of a scam — full stop.

The offer is vague on details. Genuine loan offers include clear terms: interest rate, repayment schedule, total cost. If the text is heavy on approval language and light on actual figures, that's a red flag.

The link doesn't match the company. If you hover over or long-press the link, the domain often has nothing to do with the company name in the text — random strings, misspellings, or unfamiliar domains.

Pressure to act immediately. Urgency is a manipulation tactic. Any legitimate financial offer will still be available after you've had time to verify it independently.

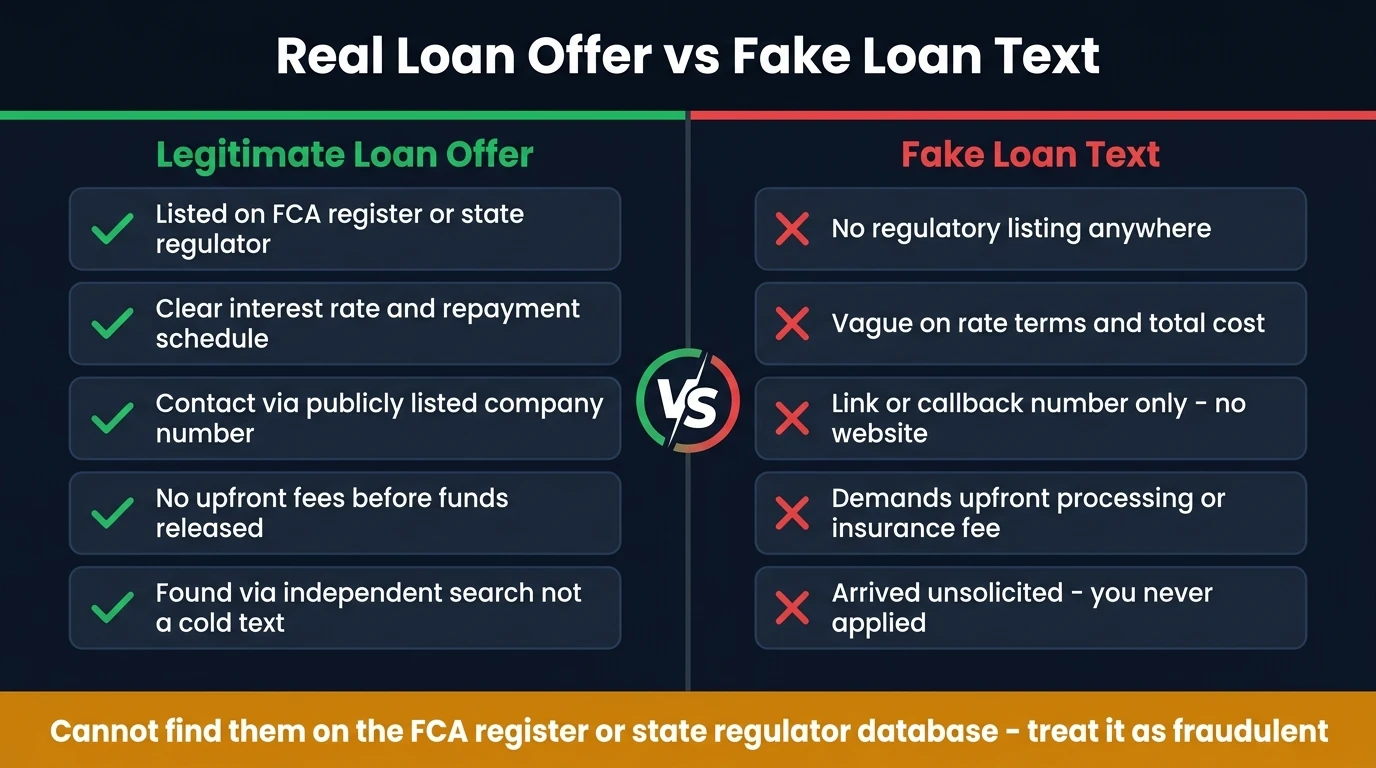

How to Tell a Real Loan Offer from a Fake One

If you ever receive a loan offer — by text, email, or phone — and you want to check whether it could be genuine, do this before clicking anything:

Search the company name independently. Don't use any contact details in the message. Go to Google, search the company name, and see what comes up. Look for reviews, regulatory listings, or consumer complaints.

Check for a licence. In the UK, lenders must be authorised by the Financial Conduct Authority (FCA). In the US, they must be licensed in your state. Search the FCA register (register.fca.org.uk) or your state's financial regulator website to confirm.

Call a publicly listed number. If the company is real, it will have a phone number on its own website — not just in the text. Call that number and ask about the offer. If it's a scam, nobody will answer, or the number won't match.

What to Do If You Receive a Scam Text

The safest response takes about thirty seconds:

- Don't reply and don't click anything — even "STOP" replies can confirm your number is active

- Block the sender immediately on your phone

- Forward the text to 7726 (SPAM) — this works on all major UK and US carriers and feeds into spam-filtering systems

- Report it to the authorities (see below)

- Delete the message

That's it. No need to engage, investigate, or try to outsmart them. The most effective response is the fastest one.

What to Do If You Already Responded

If you clicked a link, shared personal information, or sent money — act immediately:

- If you shared bank or card details: call your bank right now and ask them to flag the account for fraud. Request a new card number if needed.

- If you shared personal identity information (National Insurance number / Social Security number): place a fraud alert with the credit reference agencies — Experian, Equifax, and TransUnion. In the UK, also report to Action Fraud.

- If you sent money: contact your bank immediately about a possible chargeback or reversal. Report to Action Fraud (UK: actionfraud.police.uk) or the FTC (US: reportfraud.ftc.gov). Recovery isn't guaranteed, but acting fast gives you the best chance.

- Change your passwords for any accounts that share credentials with whatever you entered on the phishing site.

How to Report Loan Text Scams

Reporting matters. It feeds into enforcement databases that help regulators shut down these campaigns.

In the UK:

- Forward the text to 7726 (free on all major networks)

- Report to Action Fraud: actionfraud.police.uk

- File a complaint with the FCA if the scammer was impersonating a regulated firm: fca.org.uk

In the US:

- Forward the text to 7726

- File a complaint with the FTC: reportfraud.ftc.gov

- Report to the FCC: fcc.gov/consumers/guides/filing-informal-complaint

- Log the scam on the BBB Scam Tracker: bbb.org/scamtracker

When reporting, include: the date and time you received the text, the number it came from, the exact wording of the message, and any links it contained.

How Your Number Ends Up on These Lists

Scammers don't cold-dial at random — that's expensive and inefficient. They buy lists. Your phone number often gets onto those lists through the same route as your email address: data brokers.

Here's the typical chain:

- You sign up for a service using your real email address

- That service shares or sells its user data

- A data broker links your email to your name, phone number, and other details

- That enriched record gets sold to marketers — and eventually to fraudsters

The fix is to stop feeding that pipeline. Using a disposable email address for sign-ups you're not sure about means any resulting data leak contains a throwaway address, not your real contact details. That breaks the chain before it starts.

VanishInbox generates a working temporary inbox in seconds — no account needed. Use it for any sign-up you're uncertain about, and any list that's sold or leaked will dead-end at an address that no longer exists. For a full explanation of how the data broker pipeline works, see what actually happens when a website sells your email address. And for a broader look at how to protect all your personal contact details from these pipelines, see how to protect your personal information online.

A Simple Ongoing Routine

Staying ahead of scam texts doesn't take much effort if it becomes habit:

- Use a disposable email for any sign-up you're not committed to — this is the highest-impact step to reduce your presence on data lists

- Never pay upfront fees for any loan, ever — this rule alone eliminates the financial risk from every loan text scam

- Forward scam texts to 7726 before deleting — thirty seconds of effort that helps protect everyone

- Verify lenders independently before engaging with any financial offer, even ones that seem to come from a real company

- Turn on spam filtering on your phone and through your carrier — both iOS and Android have built-in options, and most carriers offer additional network-level filtering for free

For the broader picture on protecting your contact details from spam and scams, see why your inbox is full of spam — and how to stop it. For recognising the same pressure tactics when they arrive by email rather than text, see how to spot a phishing email.

Frequently Asked Questions

Is it safe to text back 'STOP' to a scam text?

No — and this catches a lot of people out. Replying with any word, including "STOP" or "NO", confirms to the sender that your number is active and monitored by a real person. That makes your number more valuable, not less. You may receive more follow-up texts or calls as a result. The correct response is to block the number and forward it to 7726 without replying at all.

Can a loan text scam affect your credit score?

Receiving the text itself has no effect on your credit score — scammers cannot run a credit check on you simply by sending a message. However, if you responded and shared enough personal information (name, date of birth, address, financial details), there is a risk of identity fraud: someone taking out credit in your name. If you think your details have been compromised, place a fraud alert with the UK credit reference agencies (Experian, Equifax, TransUnion) or the US equivalents, and consider CIFAS Protective Registration in the UK. Monitor your credit report for any applications or accounts you don't recognise.

Is CNFI USA a real company?

No regulated lender by that name is listed with the FCA or known US state financial regulators. The name is used by scammers to create false credibility. Any text claiming to be from "CNFI USA" should be treated as fraudulent.

Why does the text use my name?

Because scammers buy lists that include names alongside phone numbers, compiled from data breaches and broker records. Knowing your name doesn't mean they know anything else — it just means your contact details have been sold at some point.

I replied but didn't send money — am I at risk?

Replying confirms your number is active and monitored, which makes you more valuable to scammers. You may receive follow-up calls or texts. Block the number and monitor your accounts for unusual activity. If you shared any personal details in your reply, consider placing a fraud alert with the credit agencies as a precaution.

Can these texts install malware on my phone?

Clicking a link can potentially expose your device to malicious software, particularly if it prompts you to install an app or grant permissions. Not clicking anything is the safest approach. If you did click a suspicious link, run a security scan on your device and review recently installed apps.

Why do scammers ask for upfront fees if there's no loan?

Because the fee is the product. There is no loan — the entire operation exists to collect the fee and disappear. Once you've paid, they either vanish completely or continue to extract more money through follow-up requests ("insurance", "taxes", "legal clearance").

Should I try to waste the scammer's time to protect others?

It's tempting, but not recommended. Engaging — even to frustrate them — keeps you in communication and may escalate the situation. The most effective response is to report and block. That's genuinely more useful than any conversation.